![]() From Rome, Italy

From Rome, Italy

“I’m delighted to announce that G7 finance ministers today, after years of discussions, have reached a historic agreement to reform the global tax system, to make it fit for the global digital age and crucially to make sure that it’s fair, so the right companies pay the right tax in the right places…”. In this way the Chancellor of the Exchequer Rishi Sunak has announced the agreement among Ministries of Finance of the Group of Seven (G7).

Introduction

The agreement, signed on the 5th of June by France, Italy, Germany, Canada, Japan, United Kingdom and United States of America, deals with the adoption of a 15% global minimum tax on the profits of multinational companies worldwide. The aim of this deal is to reduce the fiscal elusion of big companies, in particular Big Tech ones, and to avoid an unfair fiscal

competition among countries, the so-called “fiscal dumping”.

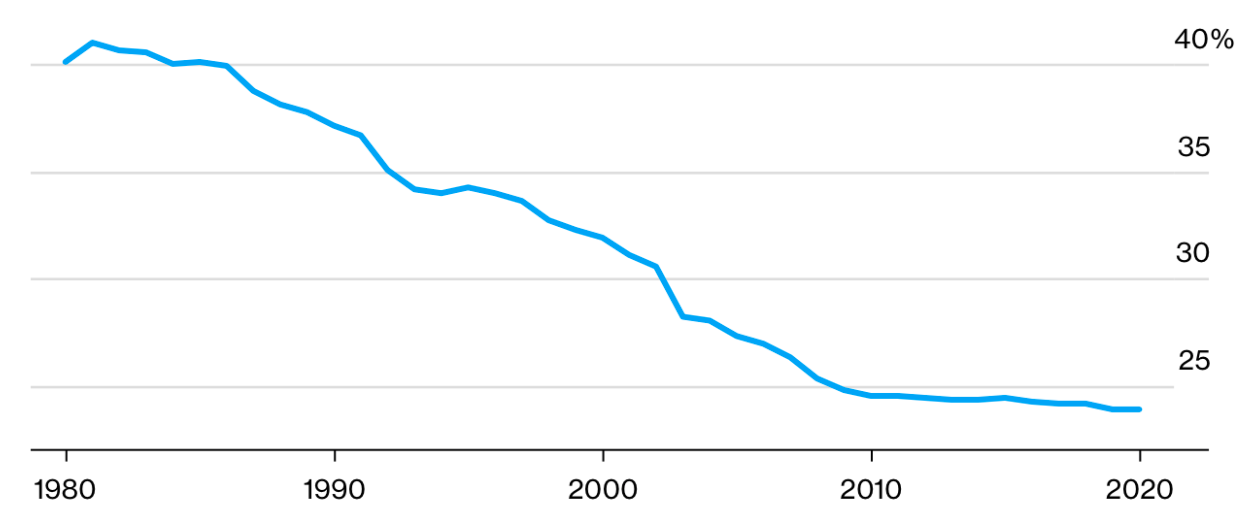

Nowadays, the global fiscal system is not adequate to face globalization and the digitalization of the economy. As shown in the graph below, the average statutory corporate income tax rates have been declining since 1980, to an average of less than 25%.

Worldwide average statutory corporate income tax rates

(source: Tax Foundation via Atlantic Council)

Moreover, another challenge the global fiscal system has to face concerns the increasing number of companies working through the internet, selling intangible products. The intangible nature of these products influences the determination of the right taxation rate, facilitating fiscal elusion.

The agreement

The deal is part of a bigger and ambitious project of international fiscal policy harmonization and is based on two main principles. The first one concerns the 15% global minimum tax, using the “country-by-country” standard. For instance, if a US company pays a tax rate of 10% in its tax residence country it will be forced to pay the remaining percentage (5% in the case) in the US, thus paying 15% globally on the profits.

The second one gives the right to the countries to set a tax rate of at least 20% on profits exceeding a 10% margin for the largest and most profitable multinational enterprises.

Revenue Forecast for Europe and Italy

Despite the agreement reached about the 15% minimum tax, the debate is still open. Nevertheless, several countries (such as France) and institutions like the EU Tax Observatory think that a global minimum tax rate of 20% or 25% would be more effective.

A study published in June 2021 by the same EU Tax Observatory projected that a 15% rate could generate for the United States the equivalent of 40,7 billion euros (49,9 billion dollars), while for European Union members the institution estimates a greater income of 48,3 billion euros. Most of this income will be up to Belgium (with an amount of 10,5 billion).

Namely, for Italy the quote will amount to 2,7 billion. This quantity is explained by the small number of Italian multinational companies. There are some firms such as ENI that operate in 72 countries and will have to add 171,5 million euros to the 4,73 billion paid in 2019 in order to reach the minimum tax. Moreover, Enel, which operates in 15 countries, will increase its fiscal count by approximately 356,3 million euros. Another industry that will be hit by the global minimum tax is the banking one, with companies like Intesa SanPaolo and Unicredit.

So, it can be stated that for Italy, looking at the origin of these higher revenues, the objective of extending the taxation to Big Tech firms and the digital economy is not so relevant.

Political Concerns

Although this agreement has an historical importance, there are several doubts and some uncertainties about it. The first one regards the non-binding nature of the deal. Indeed, it has to be ratified by every single country of the Group of Seven after a discussion with each Prime Minister. Moreover, the agreement has been signed only by seven countries. The aim of the global minimum tax is the harmonization of the worldwide fiscal system, thus needing to achieve an agreement among nations with different fiscal systems.

Technical Concerns

Beside these political concerns, there are also technical ones. For instance, it is not clear how the tax base will be defined to determine the amount of profit taxed. The idea is to determine the tax base using the IAS/IFRS standard, but the issue is still open.

The most important uncertainties regard the definition of profits, considering the intangible assets (such as patents and copyrights) and the distribution based on a geographic criterion. The role of the intangible assets and the difficulties to understand where the profits are generated are crucial points of the agreement. Indeed, the aim is to principally hit the Big Tech companies, avoiding their fiscal elusion with some mechanism such as the transfer pricing. Furthermore, another technicality that has to be defined is the treatment of losses. In particular, every country has a specific way to manage losses, thus introducing a new tax rate would pose doubts on how to report old and new losses, with the possibility of creating advantages for some countries.

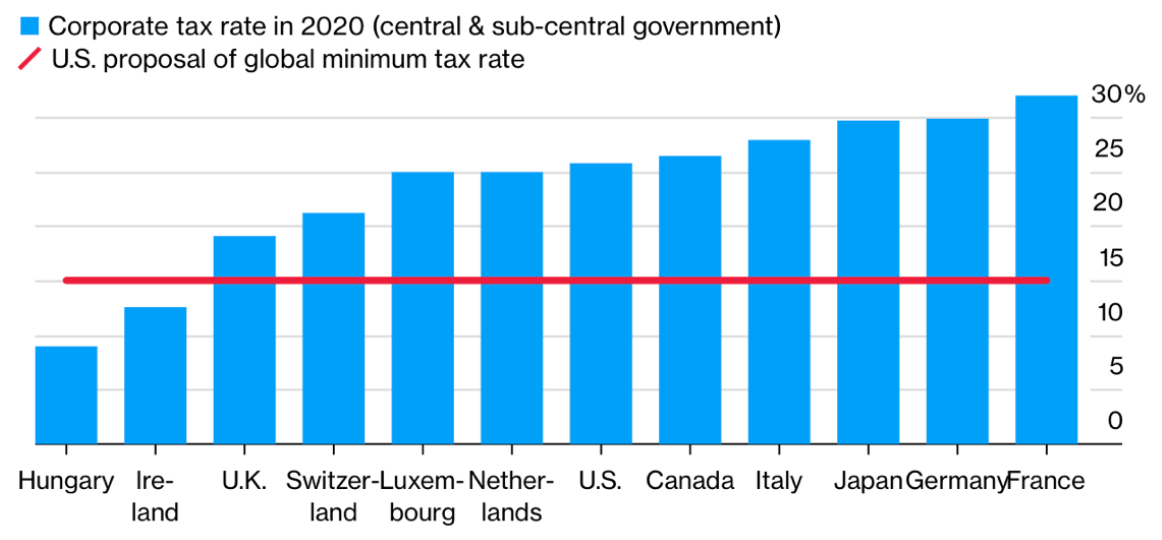

Considering the current level of taxation, it is possible to determine whether and where the global minimum tax would produce a greater impact. The OECD average tax rate on companies’ profit is now 21,5%, with only a few countries, such as Hungary, Ireland and Switzerland showing a tax rate lower than 15%, as reported in the graph below.

(Source: Organization for Economic Cooperation and Development)

Main Risks

There are some crucial risks related to the introduction of a global minimum tax rate. The first one concerns all low-income nations that have been unable so far to develop stable industries and big firms. These countries can attract foreign investors principally thanks to two expedients: the lower cost of labor and the competitive taxation. Considering the reduction of absolute poverty worldwide, with the consequence of higher wages, a more competitive fiscal system may still remain the best solution in order to attract capital and investments. As a consequence, the introduction of a minimum tax rate might reduce the competitiveness of such countries, lowering their fiscal revenues.

Another risk is linked to the market power of multinational companies. Their high market power and low-price elasticity of demand allow them to transfer this higher corporate tax on the price of their products, thus hitting final consumers.

Conclusions

Despite the agreement signed among the Group of Seven, the path towards the global minimum tax will be long and tricky. As the Italian Minister of Finance Daniele Franco said, the effective introduction of the global tax will require several years and lots of complicated agreements as well as an enormous harmonization among the different fiscal systems.

To conclude, the July meeting of the G20 will be crucial. The attendance of a big player like China might lead to more specific agreements and give a first proof of the feasibility of the Global Minimum Tax.

Bibliography

Barake M. et al., (2021). “Collecting the tax deficit of multinational companies: simulations for the European Union”. EU Tax Observatory. https://www.taxobservatory.eu/wp-content/uploads/2021/06/TaxObservatory_Report_Tax_Deficit_June2021.pdf

Bloomberg, (2021). “Historic Global Tax Deal Nears as G-7 Seeks Agreement on Tech”. https://www.bloomberg.com/news/articles/2021-06-05/historic-global-tax-deal-nears-as-g-7-seeks-agreement-on-tech

G7 UK, (2021). “G7 Finance Ministers and Central Bank Governors’ Communiqué”. https://www.g7uk.org/g7-finance-ministers-and-central-bank-governors-communique/

Il Sole 24 Ore, (2021). “La global minimum tax è un passo avanti, ma la strada è ancora lunga”. https://www.ilsole24ore.com/art/la-global-minimum-tax-e-passo-avanti-ma-strada-e-ancora-lunga-AEWwfCP?refresh_ce=1

Il Sole 24 Ore, (2021). “Tassa minima globale: per l’Italia entrate potenziali da 2,7 miliardi”. https://www.ilsole24ore.com/art/tassa-minima-globale-l-italia-entrate-potenziali-27-miliardi-AE3JOMO

International Monetary Fund, (2019). “Corporate Taxation in The Global Economy”. IMF Policy Paper. https://www.imf.org/en/Publications/Policy-Papers/Issues/2019/03/08/Corporate-Taxation-in-the-Global-Economy-46650

News pwc, (2021). “G7 commits to a global minimum tax of at least 15% and taxation of digitalised economy”. https://news.pwc.be/g7-commits-to-a-global-minimum-tax-of-at-least-15-and-taxation-of-digitalised-economy/

Pwc, (2021).”G7 Finance Ministers commit to Pillars One & Two, including global minimum tax rate of ‘at least’ 15%”. https://www.pwc.com/gx/en/tax/newsletters/tax-policy-bulletin/assets/pwc-g7-commit-to-pillars-including-min-tax-rate-of-at-least-15.pdf

Reuters, (2021). “Explainer: What is a global minimum tax and what will it mean?”. https://www.reuters.com/business/finance/what-is-global-minimum-tax-what-will-it-mean-2021-06-05/

The New York Times, (2021). “Finance Leaders Reach Global Tax Deal Aimed at Ending Profit Shifting”. https://www.nytimes.com/2021/06/05/us/politics/g7-global-minimum-tax.html

Autore dell’articolo* Federico Guerra, expert in monetary policy, markets and financial institutions of the think tank Trinità dei Monti. BA in Economics and Management at University LUISS Guido Carli of Rome.

***

Nota della redazione del Think Tank Trinità dei Monti

Come sempre pubblichiamo i nostri lavori per stimolare altre riflessioni, che possano portare ad integrazioni e approfondimenti.

* I contenuti e le valutazioni dell’intervento sono di esclusiva responsabilità dell’autore.

Editor’s Note – Think Tank Trinità dei Monti

As always, we publish our articles to encourage debates, and to spread knowledge and original and alternative points of view.

* The contents and the opinions of this article belong to the author(s) of this article only.